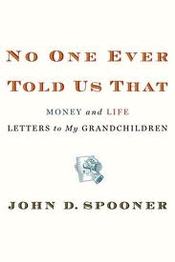

I believe in the wisdom of older people regardless of wealth or educational background. (Most) old people are precious, you can't buy their life experiences, you can only hope to share in some of them. In this book, John D. Spooner shares a series of letters that he has written to his grandchildren to prepare them for "life" Both my grandfathers died before I was even two so I took to thinking of JD Spooner as a sort of surrogate grandfather, or papa as his grandchildren refer to him, as I read this book. I won't go into detail regarding all the examples he gave, however, I would like to share the following lessons I got from the book in the hopes that one or two might touch you. These are not exact quotes, they are just notes I took as I listened to the audiobook.

This book is a bible for the ups and downs of modern day life and it doesn't take long to read! The audio version is only five hours.  If you don't get any of the above, get the book, it will be one of the best "investments" you make all year. Some of my thoughts: I disagreed with his property investing strategy. He paid all cash when, I think, the genius of property investing in the developed world lies in leverage, using other people's money - but that's another blog on its own. When he covered bonds, JD Spooner didn't cover index-linked bonds, linkers. He simply said that it is equities that keep up with the cost of living, however, Linkers also keep up with inflation. Perhaps this was taking a step too far into high finance. In the section on staying in touch with his past, JD Spooner talked about a friend of his from high school that was a plumber in a town that he moved to. He called the guy to help him out with his plumbing. I wondered, how does he feel when he's in touch with people from his past that haven't achieved nearly as much as he has: he's a multimillionaire investment advisor and author of several bestsellers. In this book, "papa" talks about owning several million dollars of Citigroup stock before it tanked and that would only be one stock in an extensive portfolio, I expect. His friends must revere him, how does he relay to them that he's still the same old guy? This is the only query that remained outstanding by the time I finished the book.

4 Comments

THE CLEVER GUYS THAT SAW THE CRISIS COMING Dr Michael Burry Michael Burry, founder of Scion Capital was the first person with a strong enough opinion of how crap subprime mortgage bonds were to buy insurance against them in the form of CDS (credit default swaps). I have written a separate blog about Michael Burry. Greg Lippmann at Deutsche Bank and his quant Eugene Xu Greg Lippmann ‘bought’ Mike Burry’s view and Michael Lewis likens him to patient zero in an epidemic. He’s the guy responsible for spreading the news that subprime mortgages were going to ‘blow-up’. Their ratings and their pricing didn’t make any sense. They were illogical, based on the wrong assumptions. Greg Lippmann reinforced the view with numbers run by his quant, Eugene Xu, described in the book as the second smartest guy in China. I loved Lippmann’s line: “I don’t have any particular allegiance to Deutsche Bank, I just work there.” Classic. Most investors who heard Lippmann’s spiel weren’t comfortable enough with the idea to short subprime. Lippmann, Xu and a few others have since started their own hedge fund, Libremax Capital, LLC.  THE CAUSE OF THE FINANCIAL CRISIS Michael Lewis goes through how the creation of financial instruments composed of money lent to people who could never afford to pay the credit back eventually led to the crisis: subprime mortgage bonds and collateralized mortgage obligations, CMOs. Mortgages were made irresistible with low ‘teaser’ rates, no need for a down-payment and, as though that wasn’t enough, no requirement for proof of income. Credit rating agencies on their behalf overrated the securities. They didn’t have access to the underlying mortgage data and were ‘too scared’ that ‘excessive’ demands for more information would lead banks to go to another rating agency taking away their fees. The rating agency models, too, were riddled with nonsensical assumptions.  WHO WERE THE BIG SUCKERS THAT WERE BLIND TO THE FOLLY OF SUBPRIME? Notable characters identified by Michael Lewis as failing to see the extent of the pending crisis in addition to rating agencies are Howard Hubler who lost Morgan Stanley a shed load of money and the CEO of AIG, Joe Cassano who ruled the company like a dictator. Overall I had two main disagreements with this book: Lewis tarnished every banker with the same brush. It’s true that desks dealing in subprime took massive risks but they account only for a very small number of people that work in investment banks. You can’t blame every single banker for subprime because bankers that didn’t deal in subprime probably knew as little as a layman about the asset subclass. You can blame the CEOs of these banks because they are meant to maintain oversight. You can also blame the individual traders that made these investment decisions. I disagreed with Lewis’s conclusion that allowing investment banks to list publicly led to excessive risk taking and hence their downfall. I think the incentive structure is the ultimate issue. Short-term profits are desired a lot more than long-term gains. Once people are incentivized to account for the long-haul performance of the financial industry should improve. My recommendation? If you want to understand the 2007-2009 financial crisis: buy!  Steve Eisman Steve Eisman Frontpoint Capital: Steve Eisman, Vincent (Vinny) Daniel and Danny Moses In many ways these were my favorite characters in the book. They, after much persuading and analysis agreed with Lippmann’s view that subprime asset back securities were overrated and overpriced so they put their money where their mouths were and bet on their demise. I found Eisman especially amusing because he said the most random things. Whenever he encountered anyone who he thought was stupid he shorted whatever they were invested in. He shorted Wing Chau (who is now suing Michael Lewis for character defamation) and a host of top Wall Street entities: Moody’s, B of A, Citi and Merrills to name a few. His reason for shorting Merrills was that whenever something goes bad Merrill is always there. Cornwall Capital: Jamie Mai and Charlie Ledley These guys started a hedge fund, Cornwall Capital, with only USD110,000. They came to the realization of subprime products quite late. However, they did something different: whilst the first movers bet on the very worst BBB subprime mortgages, they bet on the better-rated AA layer because by that point it was clear that even that layer would fail. The bet paid off by tens of millions. This is a 5* book. It’s very difficult to write a non-fiction, financial saga and actually make it interesting and readable but Michael Lewis has managed to do just that in The Big Short. The book tries to grapple with why the financial crisis of 2007-2009 happened, who saw the crisis coming and what might happen now.

|

By Heather Katsonga-WoodwardTime allowing, I love to read. If I read anything interesting, I will blog about it here. Categories

All

Archives

November 2015

|

RSS Feed

RSS Feed